Spotify through a Systems Intelligence Lens

A systems reading of one of the world's most widely taught business school cases.

The Spotify story has been examined from many different angles since the company disrupted the music industry in 2008. Management scholars have analysed its competitive strategy. Technologists have studied its product architecture and team structure. Business schools have used it to teach strategy and decision making.

This entry examines it through a different lens, a systems-intelligence lens: one that focuses on how relationships, dependencies, feedback effects, and accumulations shape what becomes possible over time.

The goal is twofold:

First, to explore what a systems-oriented reading of a classic business case can reveal, and what that revelation makes possible. Second, to encourage a way of thinking that moves beyond isolated decisions and short-term outcomes.

The conventional reading

Spotify is often presented as a paradox: a company that transformed music listening, scaled globally, and became the dominant streaming platform, yet struggled for years to turn that dominance into durable profit.

A conventional business-school reading explains this through Spotify’s economics. It would likely point to the deal that Spotify has with record labels, the entities that hold the rights to the music that Spotify streams. Record labels license these rights in exchange for approximately two-thirds of Spotify’s revenue, leaving it with very thin margins.

This diagnosis invites an examination of Spotify’s profitability, and leads to strategic questions such as: how can Spotify diversify its revenue beyond music streaming? How can it differentiate itself from competitors with comparable offerings? How can it reduce its dependency on the record labels? The strategic options explored: podcasts, audiobooks, price increases, cost efficiency, and AI-driven features, are all coherent responses to the situation as framed.

A systems lens asks a different kind of question: what structural conditions, dependencies, and dynamics shaped the range of decisions available to Spotify in the first place? This question does not replace the classical analysis but adds a layer to it.

Looking through the systems lens

A systems lens has a different starting point. Before asking what Spotify should do, let’s examine the context in which it operates. What is the story here? What kind of environment is Spotify operating in? and what can we learn from that environment’s behaviour?

The story

Spotify started out as a streaming platform, providing users with access to a vast catalogue of recorded music, and generating revenues through subscriptions and advertising.

But the music itself sits largely outside Spotify’s ownership. It belongs, in the first instance, to the artists and creators who write, perform, and record it, and is often controlled commercially through record labels. Three record labels, Sony, Universal and Warner, dominate this landscape and have been able to sustain expensive licensing terms that kept Spotify’s margins thin.

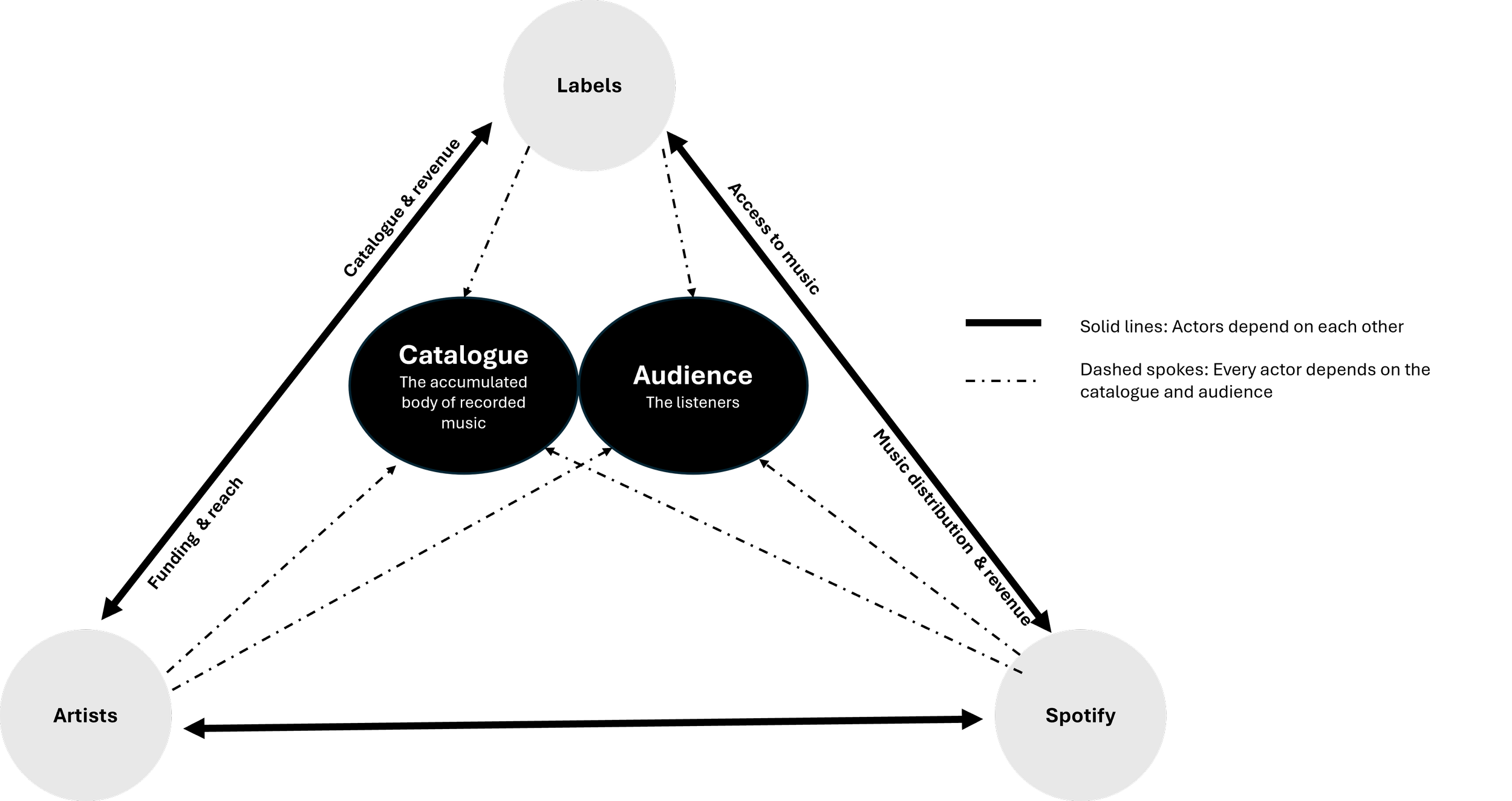

Actors and dependencies

Four actors are immediately identifiable in this story, each contributing something to the environment and each acting according to their own interests. Of course, there are more actors, and you can think of who they are later, but for the purposes of this reading, we will focus on the following actors:

Artists and creators

Record labels

Spotify

Listeners

Each actor depends on others for something essential:

Artists depend on record labels for the funding and reach that make a career in music commercially viable.

Labels depend on artists to build the catalogue that generates revenue and sustains their power in the industry.

Labels also depend on distribution channels to sell the music catalogue for profit. Streaming platforms such as Spotify, Apple Music, YouTube Music and Amazon Music, have gradually become a primary distribution channel, with 70% of the recorded music industry’s revenues in 2024 coming from streaming.

Spotify, and other streaming platforms, depend on labels for the catalogue that attracts listeners. Without the music catalogue, consumers would move to different channels, and with them the revenue from subscription and advertising.

Listeners depend on streaming platforms for convenient, affordable access to music.

Two things sit at the centre of every dependency in this environment. The first is the catalogue: the accumulated body of recorded music that every actor needs, in different ways, to fulfil their role. Without catalogue, Spotify has nothing to stream, labels have nothing to licence, consumers have nothing to listen to, and artists have no commercial presence.

The second is the listeners: the audience whose attention and payments make the entire commercial exchange possible.

A story of actors and dependencies: The story does not emerge from any one actor in isolation. It emerges from the connections among them: they each contribute and need something essential, but the music and audience hold the structure together. Without either, the whole story would collapse.

The pursuit of growth

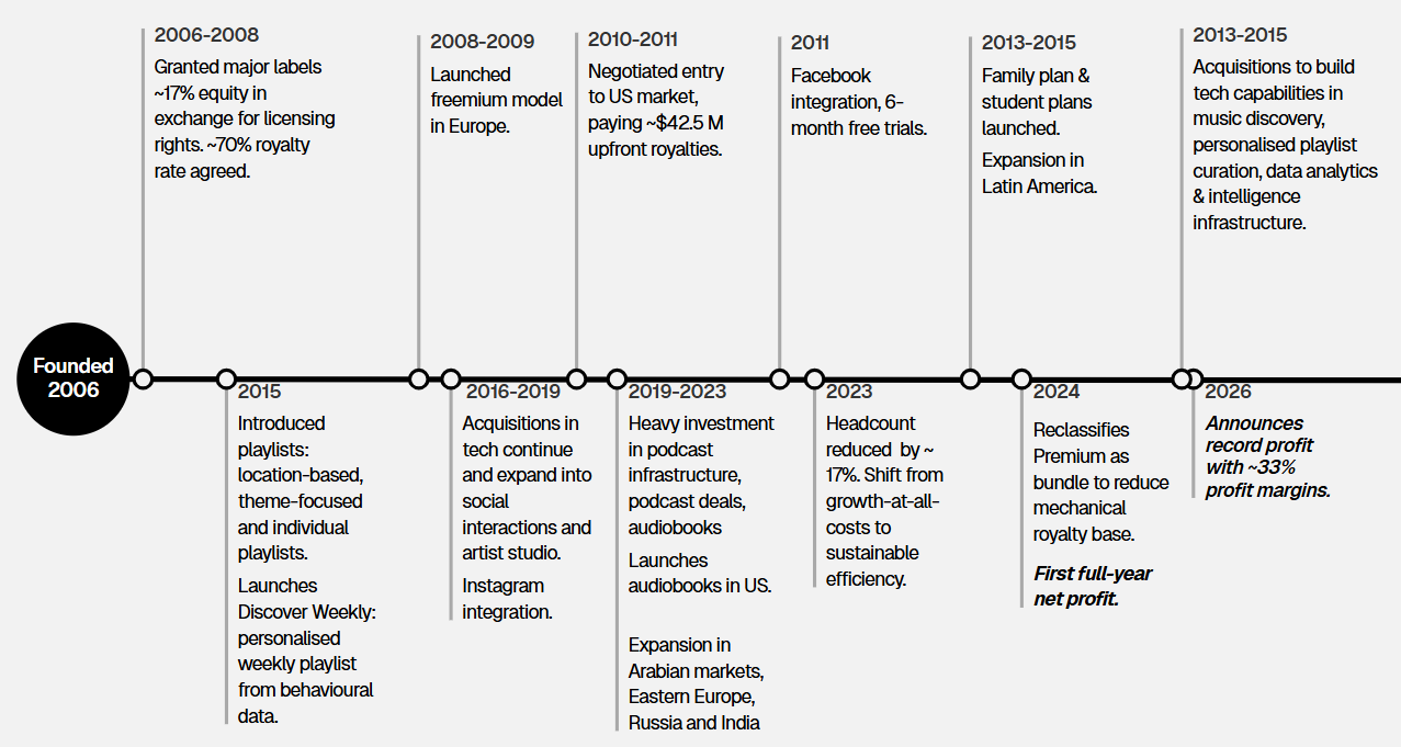

Let’s take a look at Spotify’s actions within this environment. The timeline below summarises key decisions and choices it made over time.

A timeline of documented actions by Spotify

This timeline shows that Spotify relentlessly pursued two forms of growth at once: access to catalogue and growth in audience. It spent heavily to secure music rights and expanded its user base aggressively, even when doing so came at the expense of profitability.

This is apparent across multiple decisions, including: below-cost freemium pricing that offered unlimited music for free in exchange for advertising; student and family plans priced to maximise uptake rather than margin; social media integration; massive upfront payments to record labels to enter the US market; exclusive content acquisitions designed to attract new audiences; and recommendation algorithms to increase user retention. Collectively, these moves increased Spotify’s access to catalogue, expanded its user base and deepened user engagement, with gains in each reinforcing the others over time.

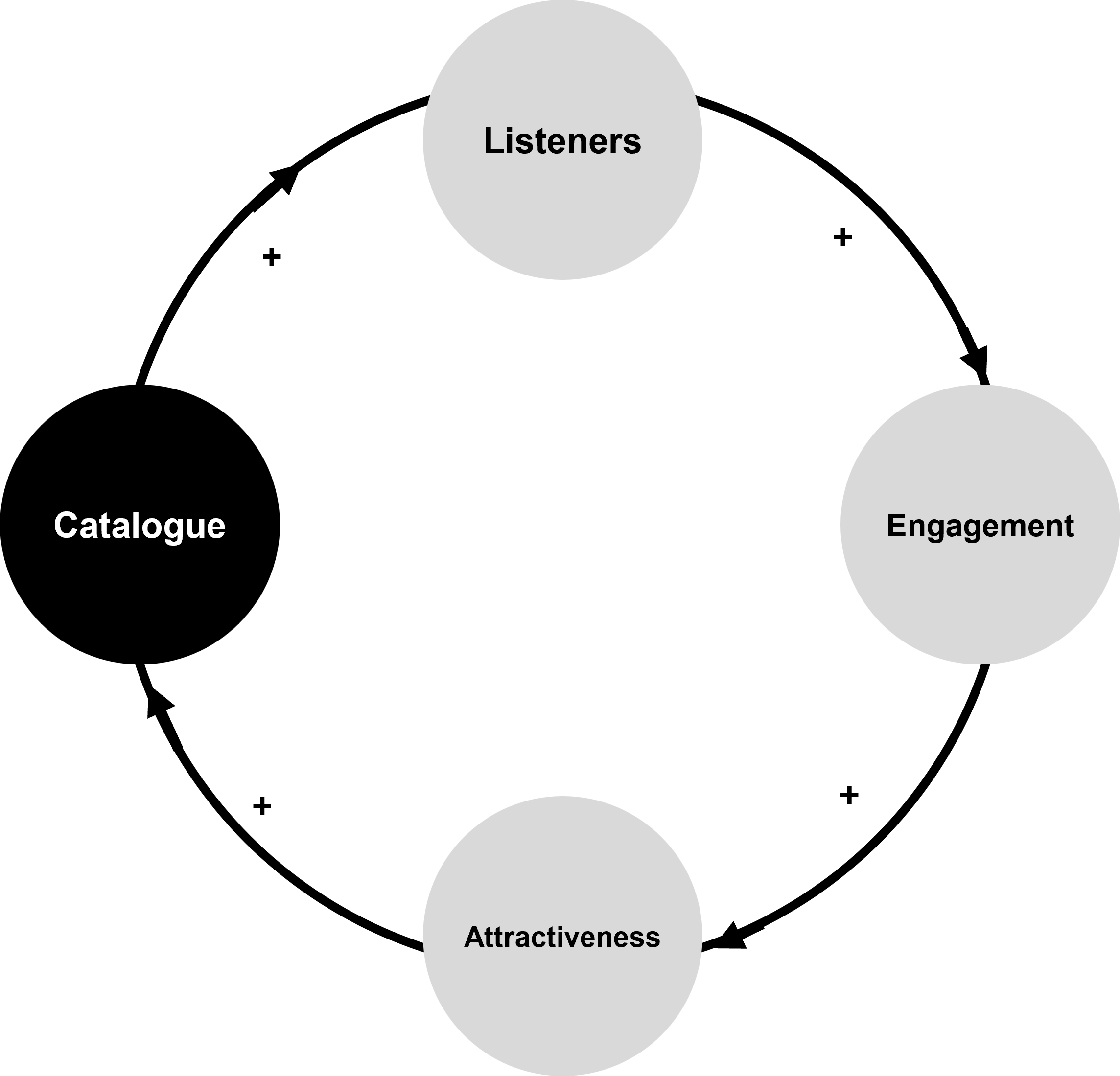

The story in motion

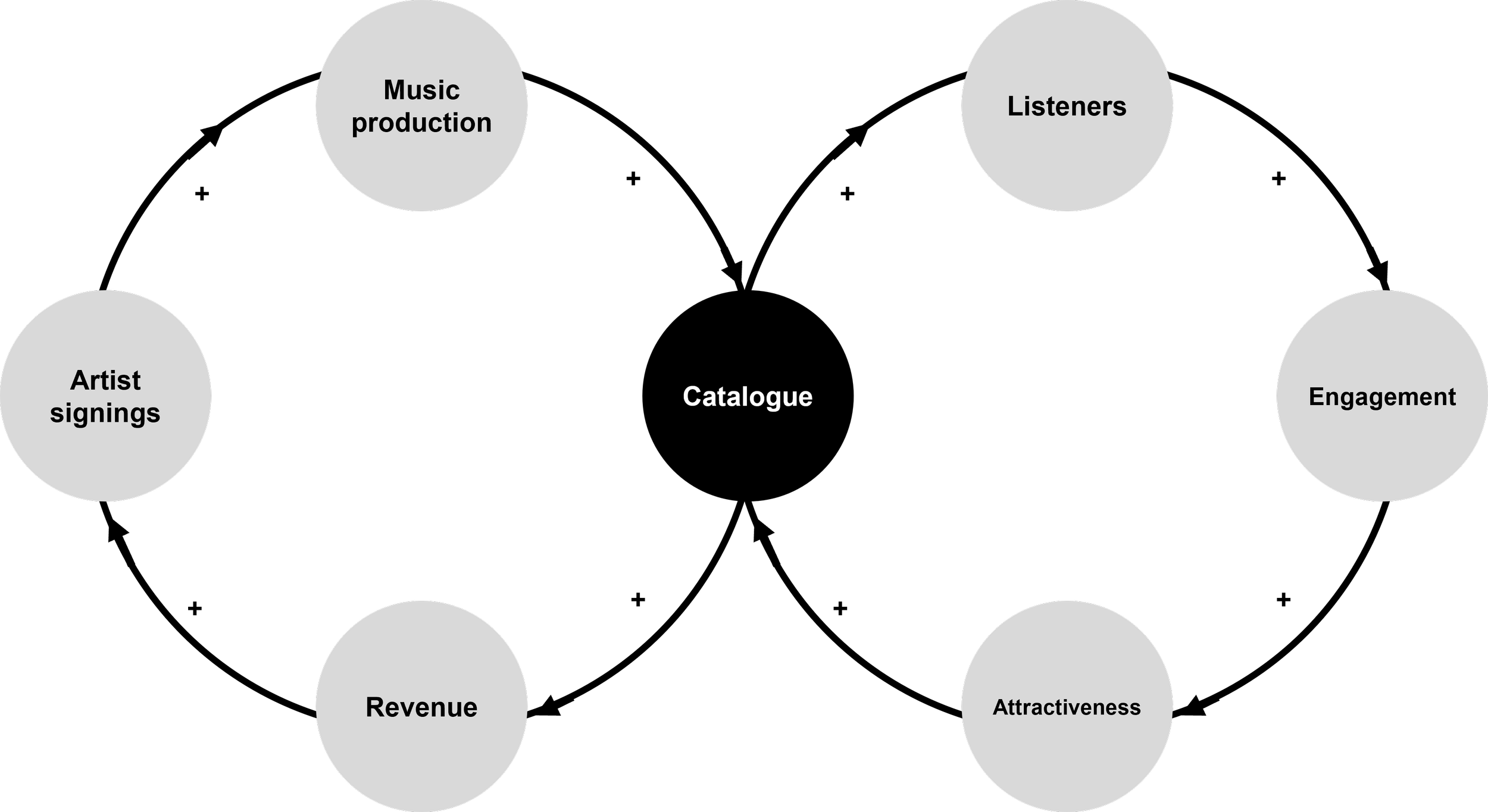

Spotify’s user base and its catalogue feed each other. A larger, more diverse catalogue attracts new users and deepens the engagement of existing ones. A larger, more engaged user base makes Spotify a more commercially significant distribution channel, making it more attractive (and increasingly essential) for artists and record labels. As artists become incentivised to promote their work on the platform, they attract their fanbase to use Spotify. The catalogue continues to grow, the user base continues to grow. The loop amplifies itself.

Spotify’s growth & catalogue flywheel:

A larger, more diverse catalogue leads to a larger and more engaged audience, which makes Spotify more attractive to creators/labels, attracting more catalogue, and further growing its user base.

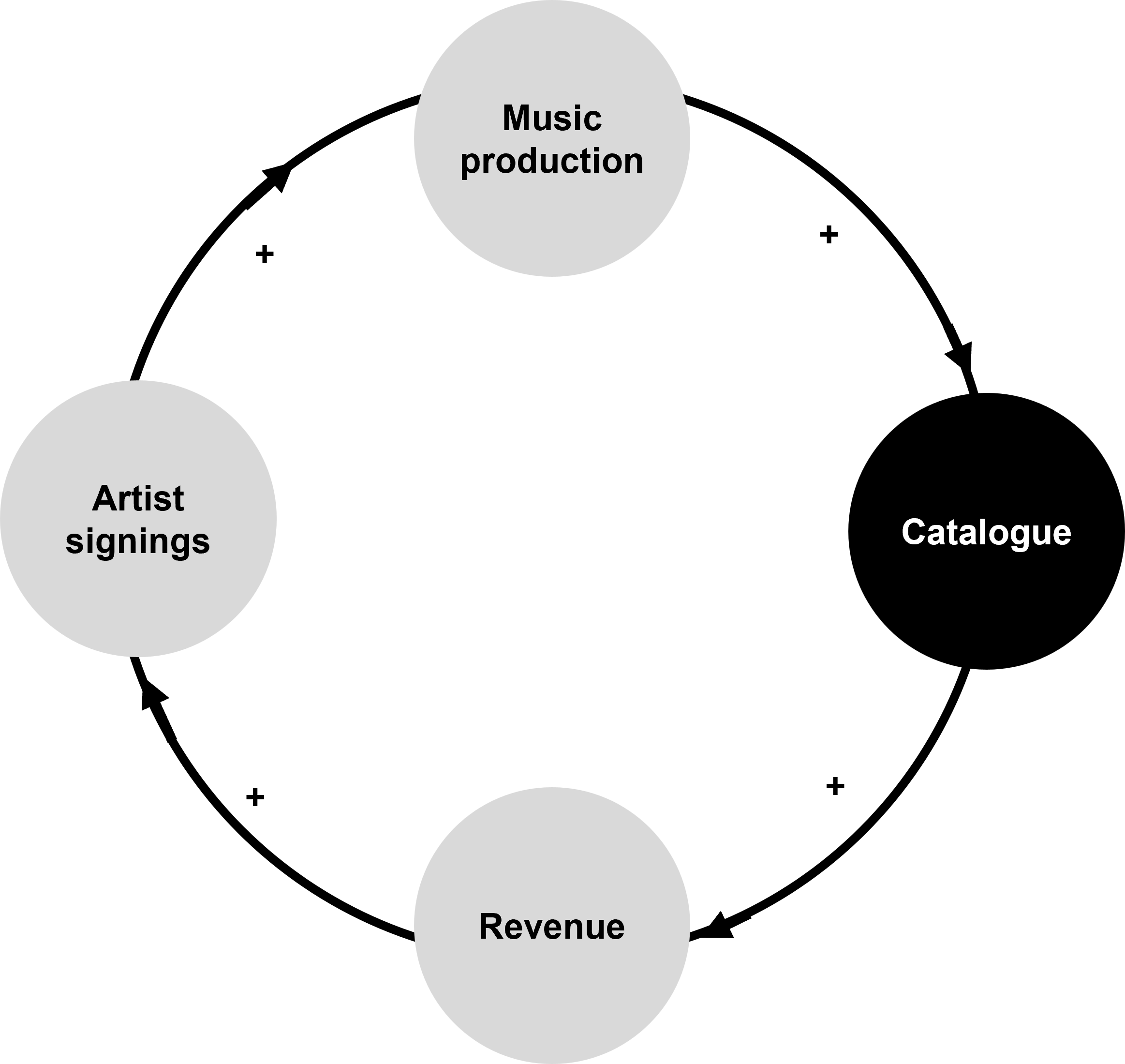

However, the flywheel depends on something that Spotify does not control: the licence to stream the music, which is largely controlled by the “Big Three" record labels.

For the labels, higher royalty revenue funds further artist signings and catalogue development, which generate more revenue. More revenue leads to more music production and more catalogue, which leads to more revenue. This loop reinforces itself too.

Record labels’ catalogue & revenue flywheel:

More catalogue leads to higher revenues, which in turn funds further artist signing, more music production and more catalogue, which brings in more revenue.

The Spotify loop and the labels loop are connected by the catalogue. Spotify depends on the labels for the catalogue, so if the labels pull or restrict access to the catalogue, Spotify’s flywheel could slow down or even collapse. Conversely, the labels profit from Spotify’s success. As Spotify’s growth flywheel spins, so does the labels’ flywheel.

Spotify’s growth strategy strengthens it as a platform, but also strengthens the Labels’ constraint on its profitability: More catalogue fuels Spotify’s growth but at the same time fuels the record labels’ ability to control a large proportion of the music catalogue. If Spotify’s flywheel spins faster, so does that of the labels.

Spotify has been operating within the constraints of this loop for much of its existence. The royalties it pays the record labels have remained high, roughly two-thirds of the revenue generated. This share held largely steady through most of the platform’s history. Why?

Because every major streaming platform needs comparable catalogue access. A platform with major gaps risks losing listeners to competitors. This has kept the labels in a strong position: they controlled the input every platform needed. The hefty royalty terms they have managed to sustain over seventeen years with Spotify reflect that position. Similarly, none of Spotify's major competitors have managed to negotiate fundamentally lower base royalty-rates. The high royalty rates became a structural constraint, and each platform selected its moves within that structure.

For Spotify, scale did not break up this position: more users generated more revenue, but also higher royalty payouts. Its entry into the large, lucrative US market did not shift it either: rather, it was met with very expensive and restricting terms. The record labels’ hold stayed strong, Spotify’s margins remained thin.

To loosen this constraint, Spotify had to build value in parts of the environment that are less dependent on the labels’ flywheel, or to change the nature of the relationship to reduce its dependence on the labels. It pursued both avenues, experimenting with other forms of audio content and investing massively into podcasts and audiobooks, which were outside of the realm of music labels. It also experimented with playlists and features to allow artists to bypass distribution via traditional record labels. Some of these initiatives were successful, some failed spectacularly. Others disappeared quietly.

New leverage

While the two flywheels were running, Spotify’s growth strategy enabled it to accumulate something less visible, a by-product of its relentless pursuit of growth: behavioural intelligence about how hundreds of millions of people discover, select, skip, share, and return to music over time.

Spotify invested heavily in the technology that powers its data capabilities. Years of this data, across hundreds of millions of users, produced a picture of human listening behaviour at a scale and specificity that is unique to Spotify. It is proprietary, outside of the record labels’ control, and compounds continuously: every user interaction adds to it, and every experiment- failed or successful- helps refine it.

Data intelligence was not the stated purpose of Spotify’s growth strategy. It was a consequence of its bet on technology, accumulating in the background. Its significance would only become apparent later, when it reached a sufficient threshold, and combined with other conditions to produce leverage that none of those conditions could produce alone.

First, there was the rising importance of digital music relative to physical music products. By 2014, digital music accounted for nearly half of the music sales globally. Subscription services were a major driver of this growth, which means that they became a critical distribution channel for record labels and artists. This was also the time when new powerful players such as Amazon and Alphabet, entered the market.

However, as most of these streaming services had catalogues of similar size, catalogue became table stakes. Spotify needed something else to differentiate and invested heavily in technology to enhance its music recommendations capabilities.

As catalogue grew, not just on Spotify but across the internet, listeners faced an increasingly frustrating problem: finding music worth hearing in an ocean of available audio.

The combination of these events, in Spotify’s specific context and at Spotify’s specific scale, produced something that neither volume nor technology nor content proliferation could produce independently. The data intelligence needed volume. The recommendation technology needed data. The content proliferation needed a solution. Combined, they became more than the sum of the parts: a highly sought-after capability unique to Spotify.

One expression of that was Discovery Mode, a feature that lets artists boost selected tracks in personalised listening contexts in exchange for a 30% commission on royalties from those streams. Another was the labels’ use of Spotify's self-serve advertising platform, Spotify Ads Manager and on-platform tools like Marquee and Showcase to promote new music, drive web traffic, and build audience engagement.

In other words, after fiercely defending the high royalty rates for over a decade, the labels began to pay some of that back into Spotify to boost and maintain visibility on the platform. Spotify was no longer a passive music distributor, it was a platform for discoverability that could provide access to audiences with precision.

Profit at last

Spotify posted its first full year of operating profit in 2024 and continued to report strong profitability in early 2026. While it is tempting to attribute that outcome to one decisive move, it can also be understood as the cumulative result of several choices reinforcing one another over time. Catalogue and audience growth, expansion into podcasts and audiobooks, years of investment in personalisation and infrastructure, and tighter operating discipline all contributed. Co-CEO Gustav Söderström framed Spotify’s confidence in similar terms: the company’s scale, technology and creator relationships were built over many years and now allow it to launch new products and monetise engagement more effectively. Decisions that once appeared costly in isolation had, together, created operating leverage and strengthened Spotify’s position within the wider audio ecosystem.

The story changes again

The environment that produced this story is not static. AI-generated music may erode some forms of catalogue scarcity, while increasing the value of attention, discovery and curation. At the same time, ownership of some of the industry's most valuable catalogues is shifting towards investment firms. These are new actors gaining prominence in this environment, and they come with different incentives. How they interact with existing actors and how existing actors respond and adapt to their presence will likely change the dynamics at play.

The structure that shaped Spotify's first two decades may not be the structure that shapes its next two. The case therefore becomes less about evaluating Spotify’s decisions individually, and more about understanding how relationships, dependencies, incentives, and accumulations interact to shape what becomes possible within an environment over time.

Alternative readings

This reading placed Spotify at the centre, starting at the same place as a conventional analysis with questions about growth, profitability, and positioning in the music-streaming environment.

But a systems reading would be incomplete with one protagonist at the centre. The story emerges from the connections among actors whose adaptive moves change the conditions facing others and produce consequences across the whole.

What would change if this story were read from another actor’s perspective? Thinking back to the dynamics and interdependencies identified here, how would the different actors strengthen, slow, or change them? And where would the resulting pressure create a new bottleneck.

The alternative readings are intended as thought provocations for the class rather than complete answers. What do these different positions add to one’s understanding of Spotify’s case?

The labels

What changes when dependence becomes mutual?

The artists

What happens when algorithms become the new gatekeepers?

The advertisers

When is Spotify selling attention rather than music?

What the systems intelligence lens opens up

The systems lens does not replace conventional strategic analysis or produce one definitive recommendation for Spotify. It changes the unit of analysis. Instead of evaluating Spotify’s decisions one by one, it examines the relationships in which those decisions operate, and asks how a move by one actor changes the conditions facing everyone else.

As the system continues to move and actors adapt, constraints can weaken, shift, or reappear elsewhere, while new opportunities and unintended consequences emerge. Spotify helped address the problem of convenient legal access to music, but this strengthened its dependency on catalogue owners. As catalogue became abundant, discovery became scarce. Recommendation systems addressed discovery, but also encouraged artists to adapt to the signals those systems rewarded. AI may reduce the constraint on content creation while making authenticity, trust, attention, and signal quality more scarce. Genuine value has been created, but the location and nature of the bottleneck have changed.

Spotify’s investments in podcasts, audiobooks, recommendation systems, advertising tools, and personalisation can therefore be read as more than a series of diversification decisions. They were attempts to alter its dependencies, build value in areas where the labels’ control was weaker, and create new strategic options. Some succeeded, some failed, and some produced consequences that only became visible much later.

The conventional question remains important: how can Spotify improve its profitability and competitive position? The Systems Intelligence lens adds further questions. What is accumulating beneath the visible results? What is being depleted? Which relationships and feedback effects are being strengthened? How is an intervention changing the conditions facing other actors? Where is the bottleneck moving? And could the strategies that strengthen Spotify today gradually weaken the resources on which its future advantage depends?

The value of the systems lens is therefore not that it produces a cleaner answer. It produces a fuller view of an environment that remains in motion, and within which any answer has to work.

Teaching this case

This case is designed to complement, rather than replace, conventional strategy analysis, inviting participants to examine the relationships, dependencies and feedback loops beneath the decisions.

The accompanying teaching note walks through suggested discussion questions, timing for a 60- or 90-minute session, and a facilitation sequence that introduces the systems lens. The materials are not intended as a comprehensive systems analysis (that would be too long), but rather as a vehicle for systems intelligence to develop in the learners.

The teaching pack includes: the case in full, all alternative readings, and the facilitator's teaching note.

Interrogate the case yourself

This case, its sources, and the systems-intelligence framing are loaded into a NotebookLM notebook. Use NotebookLM to challenge the assumptions, test the diagrams against your own reading, or explore questions the case leaves unanswered.