The labels’ perspective

If Spotify sits at the centre, the labels appear as the constraint: they own the catalogue, set the licensing terms, and take most of the streaming revenue. Placed at the centre themselves, the labels look less like a constraint and more like actors adapting to a continuously changing industry.

Before streaming became mainstream, the music industry operated under a model in which fans bought physical albums, and sales drove revenue for artists and labels. In the early 2000s, this model was disrupted by the rise of digital music. Digital file-sharing platforms like Napster and LimeWire enabled the illegal sharing of music, while Apple’s iTunes allowed the purchase of single digital tracks, unbundling the album. This resulted in dramatic declines in the sales of physical music products, crushing label revenues.

Spotify was founded as a response to the growing piracy problem: a start up with the mission to give people access to music conveniently and legally, providing a better service than piracy while compensating the music industry.

For the record labels, this presented an opportunity to participate in this new environment. They had strong leverage in the form of copyrights to the recorded music, the catalogue that Spotify absolutely needed to exist. The copyrights to the music catalogue enabled the labels to negotiate very favourable licensing terms and equity in Spotify. At the same time, they bypassed the need to invest in the consumer technology layer themselves (some initially did with little success). Spotify took on product development, user experience, subscription growth, and behavioural data collection.

The labels also licensed their music catalogue on broadly comparable terms across competing platforms, including Spotify, Apple, Amazon and Google. This helped preserve competition among the platforms and limited the extent to which Spotify could convert audience scale into overwhelming bargaining power.

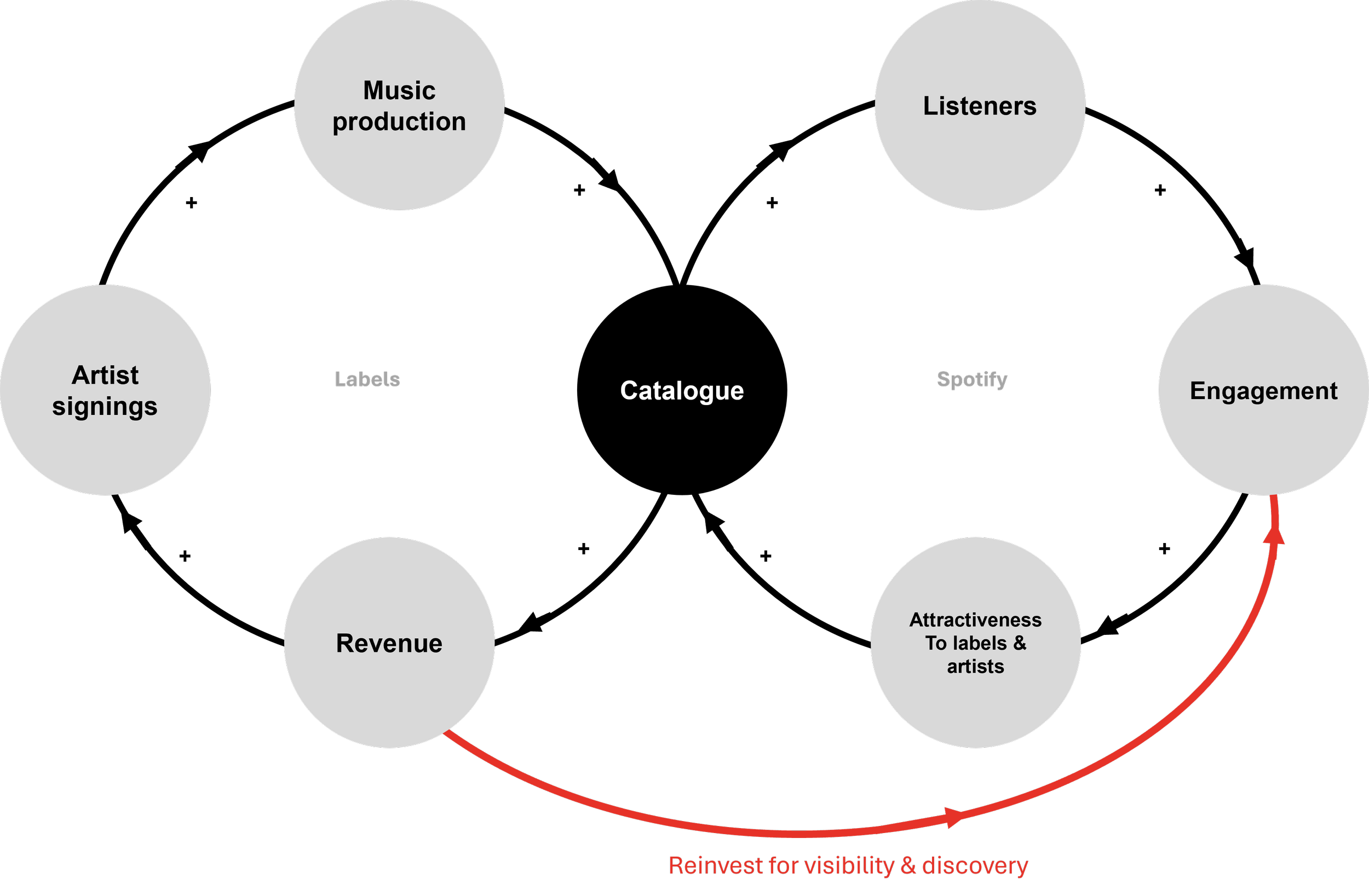

Streaming continued to gain prominence, changing how music was consumed globally. But growth brought a new problem. More artists, tracks and functional audio increased competition within the music environment. Supplying catalogue was no longer enough; labels also had to keep it visible.

Enter Spotify’s playlists. Spotify demonstrated that being included in its curated playlists like RapCaviar can significantly boost the visibility and therefore, the profitability, of a track. Labels dedicated teams solely to pitching their artists’ songs to playlist curators.

Labels also started to pay Spotify, sometimes in the form of reduced royalties, to increase track visibility through tools like Discovery Mode, Showcase and Marquee. Spotify was no longer just a distribution outlet, but a key promotional channel.

This changed the connection between Spotify’s growth flywheel and the labels’ catalogue-and-revenue flywheel. Some of the value flowing from Spotify to labels through royalties now flowed back towards Spotify in exchange for visibility and promotion. This created an additional coupling in favour of Spotify. At the same time, labels could also benefit from that reinvestment if greater visibility produced more listening, revenue, and demand for their catalogue.

Originally, Spotify depended on labels for catalogue and labels received royalties in return. Today, labels also invest in Spotify's promotional tools to increase artist visibility. The relationship has become increasingly reciprocal.

By allowing Spotify to become a primary interface between listeners and music, the labels helped it to accumulate a new source of leverage: detailed knowledge of how people interacted with, and responded to, music. Catalogue remained essential, but it was no longer the only scarce resource. Discovery, recommendation and access to attention had become valuable in their own right.

The relationship continues to evolve, going beyond licensing and promotion towards joint product development. In 2026, Spotify and Universal Music Group announced agreements for a paid tool that would allow fans to create licensed covers and remixes from the work of participating artists and songwriters. Consent, credit, and compensation are intended to be built into the product.

In this context, Spotify and the labels are not acting as adversaries negotiating over a fixed pool of revenue, but as partners combining catalogue rights, technology, audience access, and fan behaviour to create new forms of shared value. New dependencies emerge: Spotify needs rights-holder participation, while labels need Spotify’s product infrastructure and access to listeners.

Seen from the labels’ position, the story is about powerful actors using catalogue to protect their profitability, preserve competition among distributors, and remain essential while adapting to a system in which they no longer control every source of value. Their relationship with Spotify contains tension, but it is also collaborative: each holds assets the other increasingly needs.

For discussion: If labels increasingly depend on Spotify for discovery and promotion while Spotify still depends on them for catalogue, how should Spotify use that mutual dependence to strengthen its position without damaging the relationship that keeps its service viable?