The advertisers’ perspective

If Spotify sits at the centre, advertisers can look like a secondary source of revenue, mainly justifying the free tier. Put advertisers at the centre, however, and Spotify looks less like a music service and more like a market for attention.

From an advertiser’s perspective, Spotify represents an audio opportunity in a landscape dominated by visual-heavy platforms. Its appeal lies partly in the size of its audience, but also in the granular context surrounding that audience. People listen while commuting, exercising, studying, cooking, relaxing or getting ready to go out. Their choices reveal something about mood, routine and possible intent, and they are captured by Spotify.

Through this lens, a playlist is not only entertainment. It is also a source of insight that an advertiser can use. The shift described in the artists’ perspective, from music as culture towards music as mood or function, also increased Spotify’s value to advertisers.

Let’s run a thought experiment.

What if Spotify stopped advertising tomorrow? How would that impact the different actors?

The brands would likely re-allocate their budget elsewhere. They might lose Spotify’s sophisticated behavioural data but they could probably still reach similar audiences through YouTube, Google, Meta and other digital platforms. From their perspective, Spotify is one channel among many rather than a critical dependency.

The artists and labels would still need ways to achieve visibility on the platform. They may allocate their advertising budget differently, but as long as Spotify’s curated playlists and algorithmic placements continue to demonstrate value, they would still need it as a promotional channel.

How about Spotify? Here it is acting as a marketplace for attention but depends on the buyers taking part.

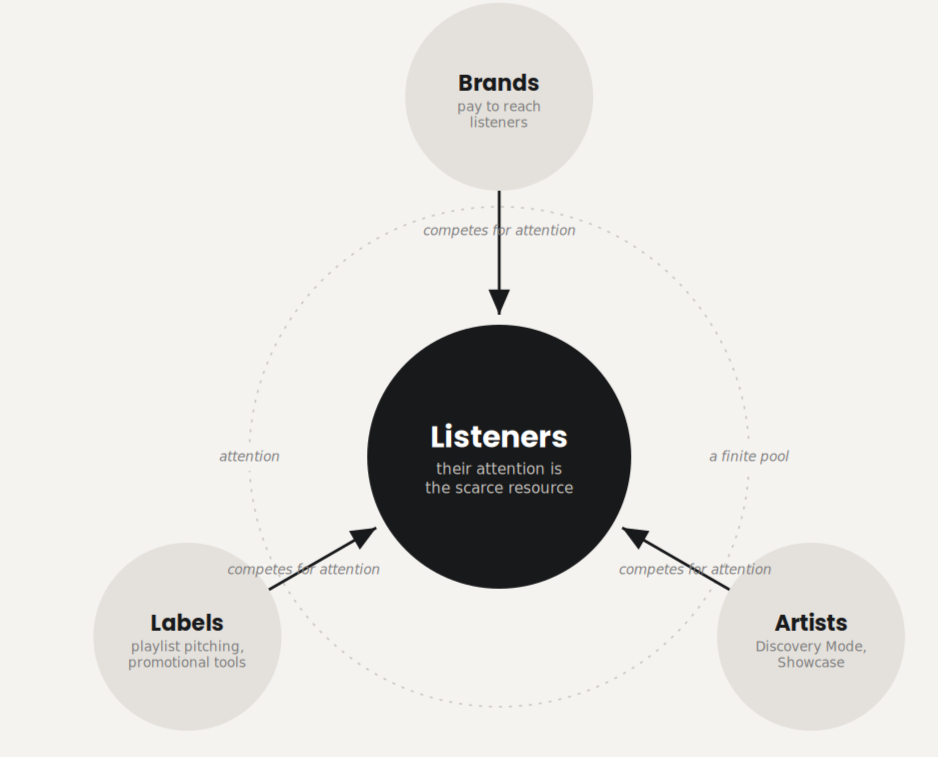

Brands, artists and labels all compete for the same finite listener attention. Spotify is the marketplace where that competition happens and it depends on these buyers taking part.

Advertising contributes roughly 10% of Spotify’s revenue. What if that marketplace collapsed? Would the revenue loss have a big impact on profitability? The advertising revenue helps justify and support the free tier, and it also serves as a form of friction to make the premium subscription more attractive. So if the advertising was gone, would the platform need to find other ways to support the free tier, which represents 62% of its user base? Would it pursue the conversion to premium subscriptions more aggressively? Or would it shrink its free tier in order to reduce the associated costs?

The answer depends on what the free tier is to Spotify: a line of revenue, a funnel towards premium, or the source of the behavioural data that gives Spotify its advantage? Each answer suggests a different decision, and a different future for the platform.

Let’s return to the listeners at the centre of Spotify’s growth flywheel. A larger free audience creates more attention and behavioural data. Better data improves targeting and measurement, which can attract more advertising revenue and help support continued free access. But the relationship contains a limit: if advertising and paid promotion weaken the listening experience or trust in discovery, Spotify may begin to drain the engagement and data quality on which the advertising opportunity depends.

For discussion: If brands, labels, and artists are all buying access to the same listener attention, how does Spotify balance advertiser value, paid promotion, and user trust without weakening the experience that makes the platform valuable in the first place?